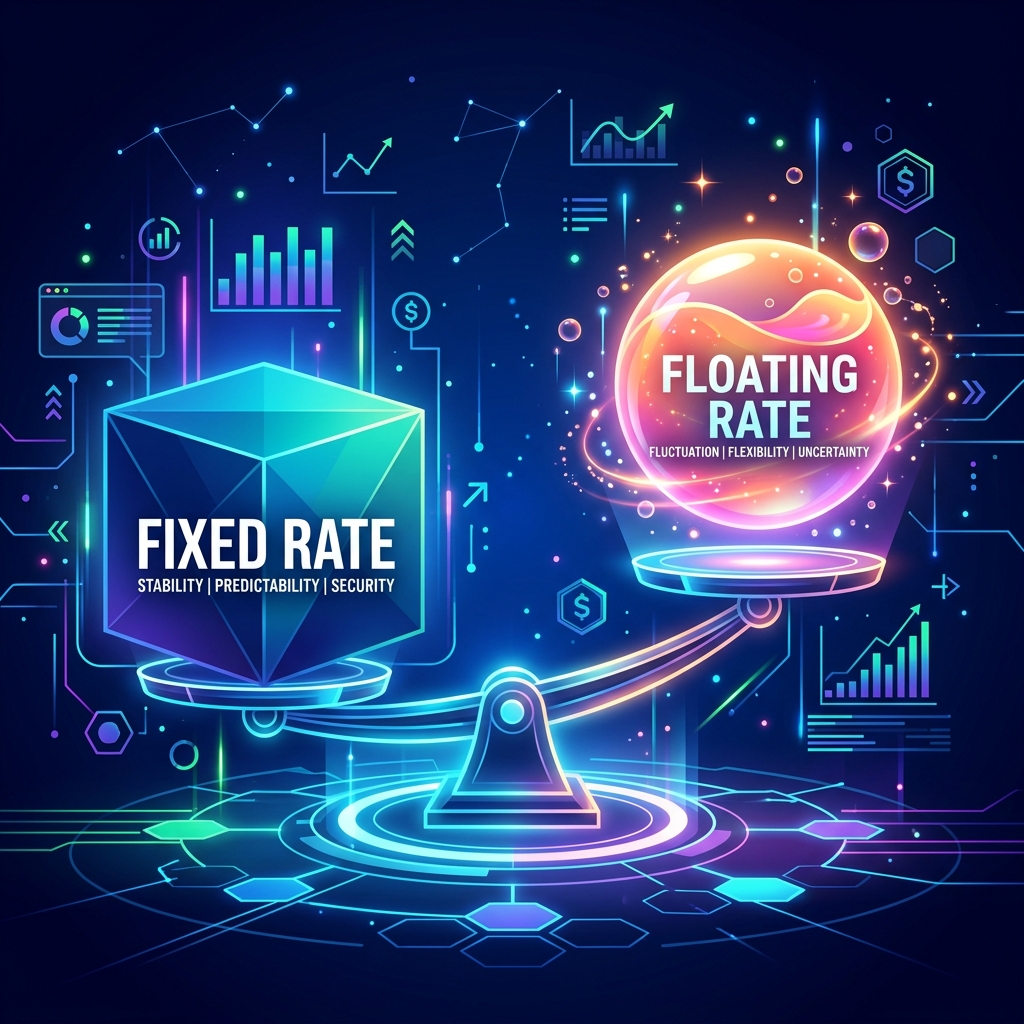

With Central Bank policy changes and global market fluctuations, choosing between fixed and floating rates is crucial. Here's a data-driven comparison.

The Evolving Global Landscape of 2026

The year 2026 has brought about a unique set of global economic conditions. After several years of global inflationary pressures and subsequent rate hikes by central banks, including the US Federal Reserve (Fed), the European Central Bank (ECB), and the Bank of England (BoE), we are now entering a phase of stabilization. For the average borrower worldwide, this raises a million-dollar question: Should I lock in a fixed interest rate now, or ride the wave with a floating (variable) rate?

⚡ Stop Guessing Your Payments

Use our global calculator to see the REAL cost of your loan instantly.

Calculate Your Real EMI Now →This decision is particularly crucial for long-term borrowers, such as those with home loans spanning two or three decades. A wrong choice today could mean paying significantly more interest over the next 20 years. In this guide, we'll deep dive into the mechanics of both systems, look at the 2026 global economic forecast, and help you decide which path fits your financial profile.

1. Understanding Fixed Interest Rates

A fixed interest rate, as the name suggests, remains constant for a specified duration of the loan. This duration could be the entire tenure of the loan or a set period (e.g., the first 5 or 10 years), after which it usually converts to a floating rate. This is common in many "teaser" or "hybrid" loan products globally.

The Pros:

- Budgetary Certainty: You know exactly how much you need to pay every month. This is ideal for salaried individuals with fixed monthly income and strict budgets.

- Protection Against Rate Hikes: If the global economy faces a new shock and Central Banks increase base rates to combat inflation, your EMI remains untouched. You are effectively "insured" against market volatility.

🌍 Plan Your Global Finances Smartly

Know exactly what your EMI will be before stepping into the bank.

Check Global Rates & Calculate →The Cons:

- Higher Starting Cost: Fixed rates are typically higher than floating rates at any given time. This is the "premium" you pay for certainty.

- Inflexibility: If interest rates fall in the future, your EMI will not decrease automatically. You would have to pay a significant "refinancing" or "switching" fee to move to a lower rate later.

2. Understanding Floating (Variable) Interest Rates

Floating interest rates are linked to an external benchmark, such as the SOFR in the US, EURIBOR in Europe, or base rates set by respective central banks. When the benchmark moves, your loan rate moves.

The Pros:

- Lower Starting EMI: Floating rates are almost always cheaper than fixed rates at the outset. This allows for better cash flow in the early years of your loan.

- Automatic Benefit from Rate Cuts: When Central Banks lower interest rates to stimulate the economy, your loan interest rate drops automatically.

- Flexible Prepayments: In many jurisdictions, floating-rate loans carry zero or very low prepayment penalties, giving you the freedom to close your loan early whenever you have surplus funds.

🛡️ Borrow Smart, Pay Less Anywhere

Compare loan tenures across currencies and see how much you save by choosing the right plan.

Calculate Personal Loan EMI →The Cons:

- Unpredictability: Your EMI or loan tenure can increase if base rates rise. This can lead to financial strain if you haven't budgeted for higher payments.

3. The 2026 Macro-Economic Context

To make a data-driven decision in 2026, we must look at the current economic indicators that are shaping the global market:

- Inflation Trends: Global inflation has started to cool down toward target ranges. This suggests that the cycle of aggressive rate hikes seen in previous years is largely over.

- Base Rate Outlook: Most financial analysts predict that Central Banks will maintain a "pause" or introduce potential small rate cuts in the latter half of the year as they pivot toward supporting economic growth.

4. Decision Matrix: Which One is Better for You?

The "better" choice depends on your specific financial situation and risk appetite. Use this matrix to guide your decision:

Choose a Floating Rate if...

- You believe that interest rates have peaked and are likely to go down or stay stable over the next few years.

- You have a "cushion" in your monthly budget to handle a 1-2% increase in interest rates if the market turns.

- You plan to make frequent partial prepayments to close the loan early.

Choose a Fixed Rate if...

- Your monthly budget is stretched so thin that even a small increase in EMI would cause financial distress.

- You are at a stage in life (e.g., near retirement) where you need absolute predictability in your outflows.

⚡ Stop Guessing Your Payments

Use our global calculator to see the REAL cost of your loan instantly.

Calculate Your Real EMI Now →Final Advice

For most borrowers globally in 2026, the Floating Rate remains a compelling choice due to the favorable economic outlook pointing towards potential rate cuts. However, regardless of which you choose, always keep an eye on your loan's "Spread" or "Margin"—the extra percentage the bank charges over the base rate. Banks often offer lower margins to new customers. Don't be afraid to refinance or negotiate!