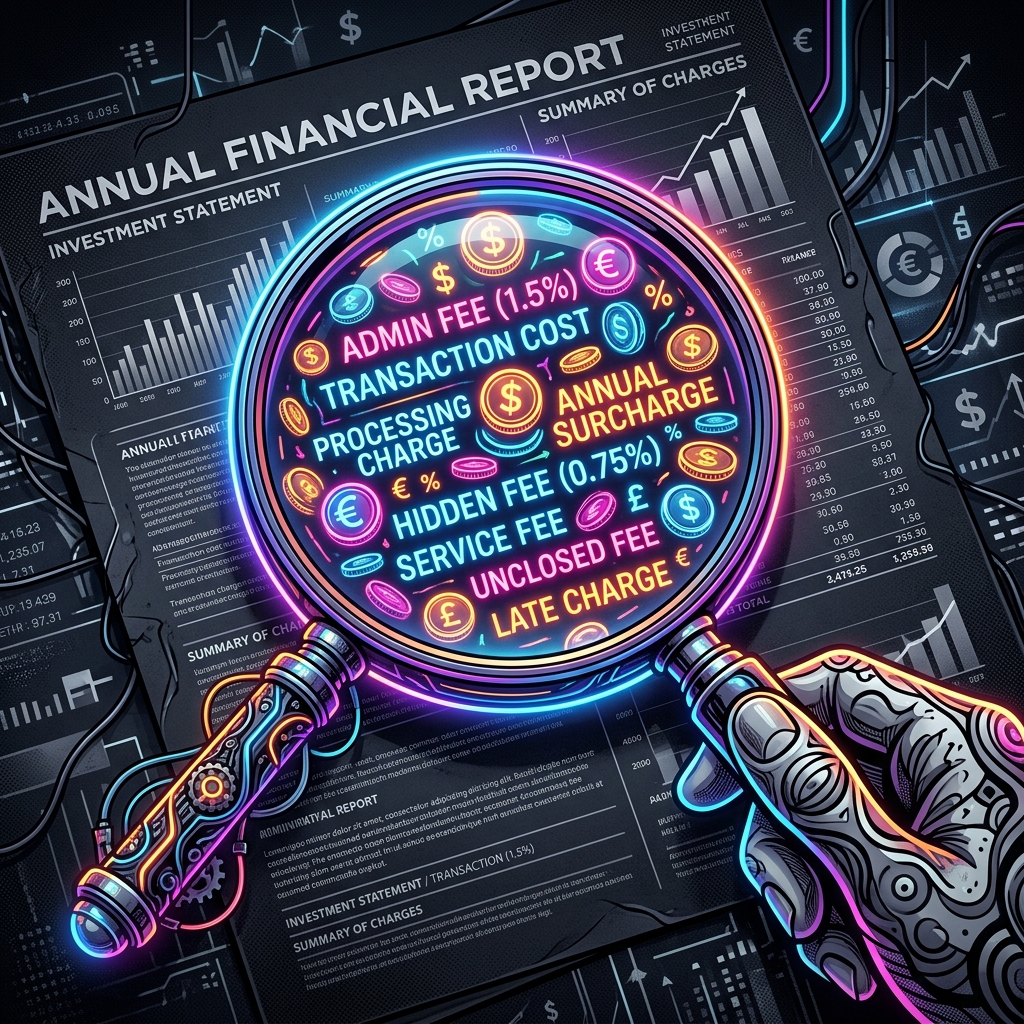

Your loan costs more than just the interest rate. Discover the hidden charges worldwide — processing fees, taxes, insurance, and more — that inflate your total cost.

The True Cost of Borrowing Globally

When you see a bank advertisement screaming "Mortgages at 5.5%!", it's easy to fall into the trap of thinking that 5.5% is the only cost you'll bear. In reality, the interest rate is just the tip of the iceberg. Beneath the surface lies a myriad of fees, charges, and taxes that can add up to thousands of dollars, pounds, or euros before you've even made your first repayment. This is why global financial experts focus on the Annual Percentage Rate (APR) rather than the quoted interest rate.

🌍 Plan Your Global Finances Smartly

Know exactly what your EMI will be before stepping into the bank.

Check Global Rates & Calculate →In this guide, we will dissect the "Hidden Costs" of loans globally so you can calculate your true APR. Understanding these will help you compare loan offers more accurately and avoid nasty surprises at closing.

1. Origination and Processing Fees: The Gatekeeper's Toll

Origination or processing fees are charged by lenders to cover the administrative costs of verifying your application, checking your credit score, performing due diligence, and legal verification. This is usually the largest upfront cost you will face.

- Typical Range: 0.5% to 2% of the loan amount. For a $500,000 mortgage, this could be as much as $10,000.

- Taxes: Remember that financial services in many countries attract VAT or sales taxes. This is often not mentioned in the initial sales pitch.

- Negotiation Tip: Banks often have promotional offers. Even without an offer, if you have a high credit score, you can often negotiate to have this fee capped or waived entirely.

2. Appraisal, Documentation and Legal Charges

For home loans specifically, the bank will hire external appraisers to estimate the property's market value and lawyers/title companies to verify the property's title deeds and ensure there are no legal disputes. While the bank requires them, you are the one who pays the bill.

These combined charges can range from $500 to over $3,000 depending on the property value, its location, and local real estate laws.

🛡️ Borrow Smart, Pay Less Anywhere

Compare loan tenures across currencies and see how much you save by choosing the right plan.

Calculate Personal Loan EMI →3. Mortgage Insurance (PMI) & Life Insurance

If your down payment is less than 20% in many countries (like the US or UK), lenders will mandate Private Mortgage Insurance (PMI) or equivalent schemes. This protects the lender, not you, if you default. Furthermore, some banks strongly suggest you take a life insurance policy covering the loan amount.

The premium is often added to your loan principal, meaning you pay interest on your insurance premium for the next 20 to 30 years. Pro Tip: Always check if you can buy a separate, cheaper term insurance policy from an independent provider.

4. Prepayment and Early Repayment Charges (ERC)

Lenders make their profit from the interest you pay over time. When you pay back a loan early, they lose out on that future profit. To discourage this, many lenders charge a fee if you pay back more than your scheduled EMI or close the loan account early.

- Check the Rules: In some regions, early repayment charges are heavily regulated or banned on certain types of loans. Always read the "Early Repayment" or "Foreclosure" clause in your loan agreement. Charges can be as high as 2-5% of the amount being prepaid.

⚡ Stop Guessing Your Payments

Use our global calculator to see the REAL cost of your loan instantly.

Calculate Your Real EMI Now →5. The Cost of Delays: Late Payment & Default Charges

Life happens, and sometimes an EMI payment might get delayed. However, the penalties are designed to be steep.

- Penal Interest: Lenders can charge high default interest rates on overdue amounts.

- Credit Score Impact: This is the biggest "hidden" cost. A single missed EMI can drop your credit score significantly globally, making all your future loans and credit cards more expensive.

Conclusion: How to be a Smart Borrower

When comparing loan offers, don't just look at the interest rate. Ask for a Closing Disclosure or a document outlining all terms and conditions. A loan with a slightly higher interest rate but zero origination fees and no prepayment penalties might actually be the cheaper option in the long run.

Calculate the APR by adding all these upfront costs to your total interest outflow. Being a smart borrower means reading the fine print and understanding that the cheapest loan is the one with the lowest total cash outflow.